China Has Been a Major Problem for 30 Years — But We Had Not Understood It

1. Now China Scares Everyone

It took the frontal offensive launched by Chinese manufacturers in the car industry to awaken a dormant Brussels. Indeed, Europe, already threatened by Trump’s tariffs and Middle Eastern adventurism, with all their consequences for energy and inflation, now sees its granite-like German-centered certainties about China as an Eldorado for the products of our continent crumbling day after day.

For more than two decades, the European Union had lulled itself into the illusion of having found in Beijing the ideal partner to turn two of its ideological paradigms into reality: making its consumers happy, along with the billion-euro balance sheets of Northern European importing traders, plus a few Spaniards, by allowing a flood of low-cost products to arrive from China, which had just entered the WTO; and making its two main founding countries, Germany and France, happy, both well pleased to export luxury cars and Airbuses to China, the new great potentially unlimited market, given its enormous size, offered to them on a silver platter by globalization.

But now that illusion has shattered. Not only because globalization is over, at least as we have experienced it so far, but also because of the change in mentality imposed on Chinese citizens by the current political leadership, which has said enough to the ostentation of European luxury and has invited its population to buy goods made in China.

The alarm sirens for the China danger, a country that in a short time has transformed from a promising market into a fearsome competitor for European industries, are now sounding continuously in Brussels, as during a bombing. In Italy, the issue of asymmetric competition and Chinese dumping was at the center of the latest Confindustria Assembly and of the report by its president, Emanuele Orsini. Meanwhile, Spain, France, Italy, the Netherlands, and Lithuania, with the notable absence of a hesitant Germany, have asked Brussels to strengthen the tools for defending European industry against the increase in “unfair trade practices” in order to face Beijing’s overproduction, which translates into a flood of Chinese goods sold below cost in the Old Continent.

A sign of this change in the common perception of the China danger, including in Italy, is the long article that Federico Fubini devoted to the topic a few weeks ago in Corriere della Sera: “China Is Eating Made in Italy, and Europe: Why Are We Afraid to Defend Ourselves?” A headline that would have been unthinkable in a major Italian newspaper even only a few years ago.

Yes, because it is worth emphasizing that, for years, most Italian intellectuals and commentators also told us that China was a friendly country and a potential golden market for Made in Italy, while our textile and footwear districts were instead agonizing under the blows of unfair competition and Chinese dumping. Those same intellectuals and commentators had also repeatedly taken positions in the past against the demand for tariffs on Chinese products made by the sectors of our industry most affected, judging that request as a backward attitude. Instead, for years they invited Italian small and medium-sized enterprises, always looked down upon by a certain domestic mainstream, to “wake up” and seize the great opportunities offered by the Chinese market rather than complain about Asian competition. A typical radical-chic attitude which, now that the China danger for the Italian and European economy has become obvious, has almost become a source of embarrassment.

2. What We Were Writing About China Several Decades Ago

The Edison Foundation, and in particular the writer, had already warned before China’s entry into the World Trade Organization in 2001 that the foreign trade of the Asian giant would create more damage than benefits for the Italian economy. Indeed, given the particular similarity between the international productive specialization of China and that of Italy at the time, when we did not yet have today’s strong pharmaceutical, cosmetics, food, aerospace, shipbuilding, and mechanical sectors, the full-sail entry of the Asian giant into free trade would have exposed us even more to Chinese asymmetric competition, plagiarism, and dumping in traditional low-cost goods such as textiles, clothing, footwear, furniture, taps, and ceramics, which had already begun to suffer Beijing’s aggressiveness from the early 1990s. This critical position of ours, shared by few Italian figures, including Giulio Tremonti, author in 2005 of the prophetic book Fatal Risks. Old Europe, China, Suicidal Marketism: How to React, was at the time branded as “neo-protectionism.”

While the Italian mainstream, on one side, praised the Silk Road and Europe, on the other side, completely ignored the impact of Chinese competition on the Italian economy, with the notorious Trade Commissioner Peter Mandelson appearing closer to Beijing’s interests than to ours, the Edison Foundation supported the National Association of Italian Footwear Manufacturers and the then Deputy Minister for Foreign Trade Adolfo Urso in obtaining anti-dumping duties from the European Union against Chinese and Vietnamese footwear. These entered into force first and were then extended a second time.

Since the beginning of the new millennium, we repeatedly denounced numerous cases of counterfeiting of Italian clothing, furniture, and tapware brands by Chinese companies, a phenomenon that continues today. We personally promoted the proposal to make the indication of the country of origin mandatory on products imported into Europe from non-EU countries, the so-called mandatory “Made in” label, which the Italian government brought to Europe. That proposal was later approved by a large majority in the European Parliament but was ultimately rejected in the Council of Europe, mainly because of Germany’s veto, since that country had by then relocated several of its productions to China.

Through various articles, we illustrated the China danger from different angles, rationalizing it mainly under two profiles. The first was to denounce the tsunami that China’s asymmetric competition, made up of social, environmental, and currency dumping, was generating on Italian manufacturing and industrial districts, with a dramatic loss of added value and jobs. The second was to curb illusions about an alleged future boom in Italian exports to China itself.

3. The Impact of Chinese Asymmetric Competition on Italian Manufacturing at the Beginning of the Century and the Illusion of China as the New Eldorado for Made in Italy

Those who still write today that our GDP struggled for a long time to recover 2007 levels may not yet have understood how much Beijing’s asymmetric competition contributed to bringing the Italian economy to its knees in that period, even before the global financial crisis of subprime mortgages, the Greek contagion on our sovereign debt, and the subsequent austerity. China, subprime mortgages, Greece, and austerity were, for Italy at the beginning of the millennium, like the four horsemen of the apocalypse, but it was China that struck the first and deadliest blow.

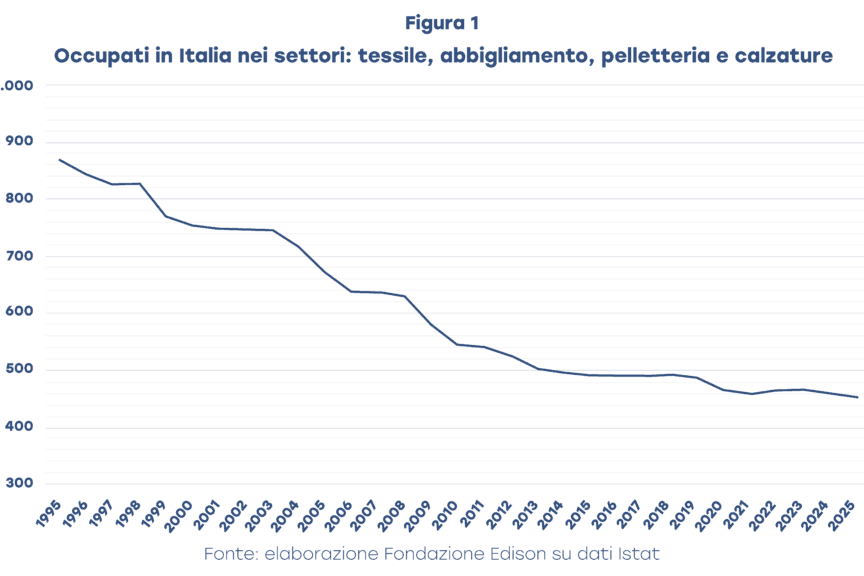

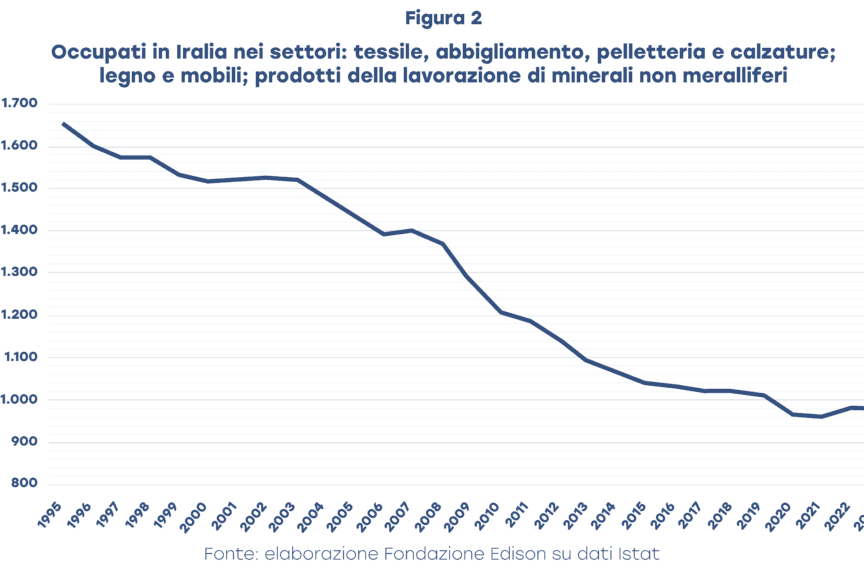

A few figures are enough to recall what happened from 1995 to 2013. According to national accounts data, Italian manufacturing industry lost 677,000 workers in just eight years. Of these, 369,000 were lost by our textile, clothing, and footwear sector: it was the greatest hemorrhage of jobs in a single national European industrial sector ever to happen in such a short time. If, to the losses in textiles, clothing, and footwear, we add those in wood-furniture and the processing of non-metallic minerals, ceramics and ornamental stones, Italy suffered an overall fall in employment in these sectors most exposed to Chinese asymmetric competition of as many as 561,000 workers, equal to 83% of the total lost by manufacturing in that period.

In those years, the Berlusconi government entrusted me with the task of preparing a preliminary report for the Second National Conference on Foreign Trade, which was held in Rome on February 26, 2005. In that report, the issue of the China danger for our economy was brought to general attention. In particular, some impressive estimates were provided on the loss of market shares suffered by Italy in Europe during those years as a result of Chinese asymmetric competition.

With regard to the impact of Chinese competition on Italy’s market shares in the world, it is interesting, for example, to analyze data concerning the European Union with 15 members, both because they are particularly accurate and up to date and because the EU-15 was Italy’s main export market, having absorbed 53.5% of our exports in 2003. Available statistics clearly show that the European market had been literally invaded in recent years by goods from China. In some cases these were goods exported directly by Chinese companies; in other cases they were goods imported into Europe by European multinationals that had relocated production plants to China; in still other cases they were goods marketed by European purchasing groups that had commissioned production from Chinese firms.

To shed light on this phenomenon, the Edison Foundation analyzed the dynamics of EU-15 imports in 16 important product categories, with particular reference to goods coming from Italy and China. These were seven product categories belonging to the “clothing-fashion” system, footwear, knitwear and socks, woven clothing and accessories, glasses, frames, goldsmithing and jewelry, leather goods, and nine product categories belonging to the “home furnishing” and “automation-mechanics” systems, taps and valves, lamps and lighting technology, furniture and kitchens, sofas and chairs, metal household goods, hardware, furniture hinges, locks and handles, cutlery and utensils, and processed ornamental stones.

Overall, in the 16 product categories analyzed, between 1996 and 2003 EU-15 imports from China grew from 9 to 22.2 billion euros, an increase of 147%, while EU imports from Italy for the same products increased over the same period by only 9%, from 17.3 to 18.9 billion euros. In the seven product categories of the “clothing-fashion” system, China had clearly become the EU’s leading supplier, with 16.1 billion euros, ahead of Italy, with 11.1 billion. China was also increasing its exports to the EU in sectors such as jewelry-goldsmithing or eyewear, where it had been practically absent eight years earlier.

The same was happening in the nine categories of mechanical and home-furnishing products examined by the Edison Foundation. In this case, Italy was more than four times more important than China as a supplier to the EU in 1996, while in 2003 the ratio in our favor had fallen to 1.2. Between 1996 and 2003, EU-15 imports from China in the nine categories of mechanical and home-furnishing products grew by 322%, from 1.5 to 6.2 billion euros, while sales of the same products from Italy to the EU increased by only 22%, from 6.4 to 7.8 billion. The largest increases in European imports from China in home goods and mechanics concerned taps, lamps and lighting technology, furniture, and ornamental stones.

It is therefore necessary to acknowledge that Chinese asymmetric and unfair competition was producing extremely negative effects on the trade balance and on the Italian productive system, weakening at its roots the very fabric of our civil society, especially in some important districts and regions of the country.

But these alarming data were not listened to very much, not only in Europe but even in Italy, because of a prevailing current of thought and lobbies that tended to downplay their relevance by opposing to them the supposedly formidable opportunities that the Chinese market would offer Made in Italy. This genuine nonsense was repeatedly criticized by me, with numbers in hand.

That China was the real economic novelty at the beginning of the 21st century was beyond doubt, but for an economy like Italy’s it was important to do the math properly so as not to overestimate its own capacities toward the Asian giant. The analysis therefore could not ignore the figures, which, however dry, warned against unjustified hopes that would loosen vigilance toward Chinese asymmetric competition and counterfeiting. This reality, as we have seen, was producing very serious consequences in our districts and in many key sectors of Made in Italy, starting with footwear and textiles-clothing.

It should immediately be clarified, to provide some terms of comparison, that in 2003 Italian exports to China, a country with 1.3 billion inhabitants, were only 17% higher than those to Portugal, a country with only 10 million inhabitants. It was therefore said that Italy was late on the Chinese market; but since our exports to China were growing strongly, one had to look to the future with optimism. However, even if Italian exports, or a mix of these and direct local sales, to China continued to increase annually at a rate of around 15% at current values, as happened in 2004 after a significant decline in 2003, in 2010 they would reach only 10.1 billion euros.

The size of this figure can be understood by observing that it is 1.7 billion lower than our then-current imports from China itself, which in 2004 should have reached 11.8 billion, and clearly lower than the amount of our current exports to Spain. This “small” country compared with China, with 41 million inhabitants, which was then tied with the United Kingdom as our fourth market after Germany, France, and the United States, had imported 18 billion euros from us in 2003. Growing at an annual rate of 15%, Italian exports to China would manage to equal current Italian exports to Spain only in 2015. Whereas, assuming that our exports to Spain grew at least 5% per year, Italian exports to China would need as many as 15 years of growth at 15% per year to equal the Spanish market in value. In other words, one would have to wait until 2020.

We were prophetic. In fact, our projections turned out to be wrong, but by underestimation. In 2025, Italy exported to China only 14.3 billion euros, just 2.2% of total Italian exports, barely one billion more than we exported to a small country like Austria, 13.2 billion, and almost 24 billion less than we exported to Spain, 38.2 billion. Therefore, China never became an Eldorado for Made in Italy, while in 2025 our bilateral deficit with Beijing rose to 46.3 billion euros, the highest we have after the much smaller deficits in value with the Netherlands and Germany.

4. The Second Chinese Shock: This Time It Affects All of Europe

What Sander Tordoir and Brad Setser, in a recent report for the Centre for European Reform, defined as the second Chinese shock, strikes the whole of Europe this time, even Germany, which has always maintained privileged relations with Beijing, exploiting the opportunities offered by the Chinese market, but now sees its key sector, automotive, threatened by China.

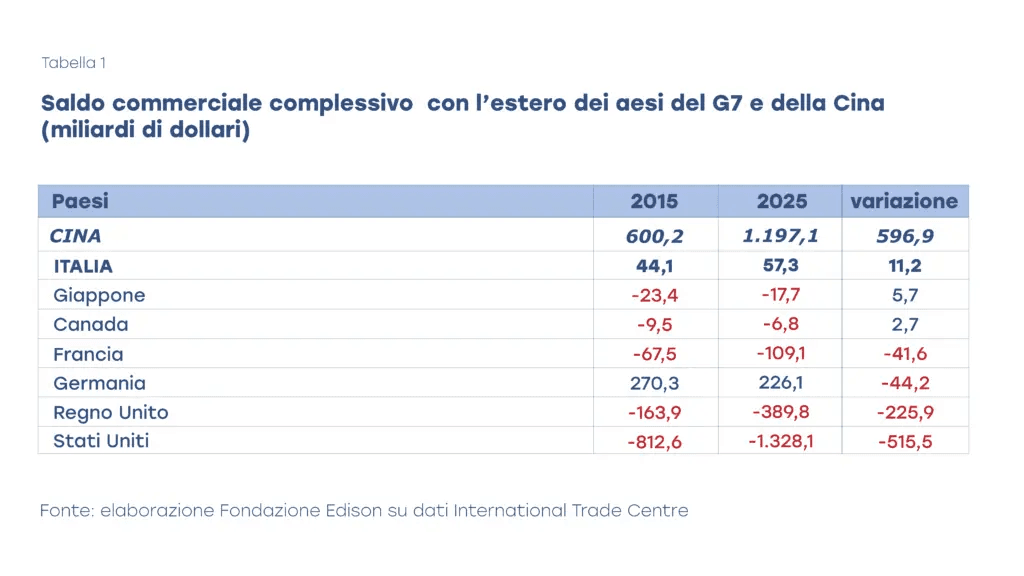

China’s trade surplus with the rest of the world reached a record level of 1.197 trillion dollars in 2025, with an increase of 597 billion in ten years compared with 2015. Among the G7 countries, Italy is the only economy that improved its trade surplus over the decade, by about 11 billion, while Germany worsened its surplus by 44 billion and France its deficit by 42 billion. Canada and Japan slightly improved their deficits, while those of the United States and the United Kingdom expanded enormously, worsening by 515 and 226 billion respectively.

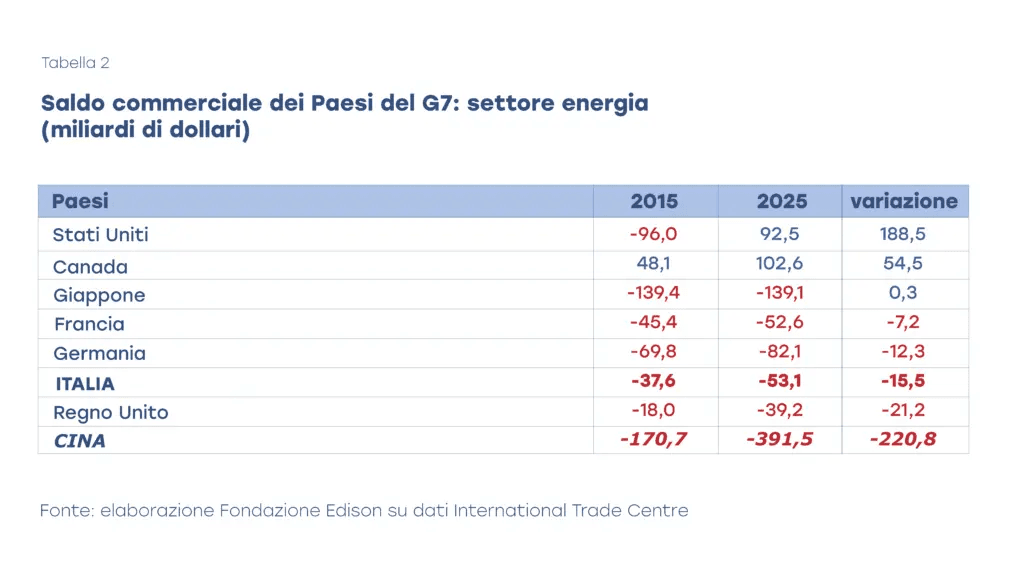

The data also highlight China’s enormous foreign trade deficit in energy, which worsened from 2015 to 2025 by 221 billion dollars. Over the same period, Canada increased its surplus by 54 billion, while the United States moved from a deficit of 96 billion to a surplus of 92 billion. Japan’s high energy deficit remained stable, while the deficits of the four European G7 countries worsened. Italy’s foreign deficit, in particular, rose to 53 billion. It should be noted that energy accounts for about 12% of world exports.

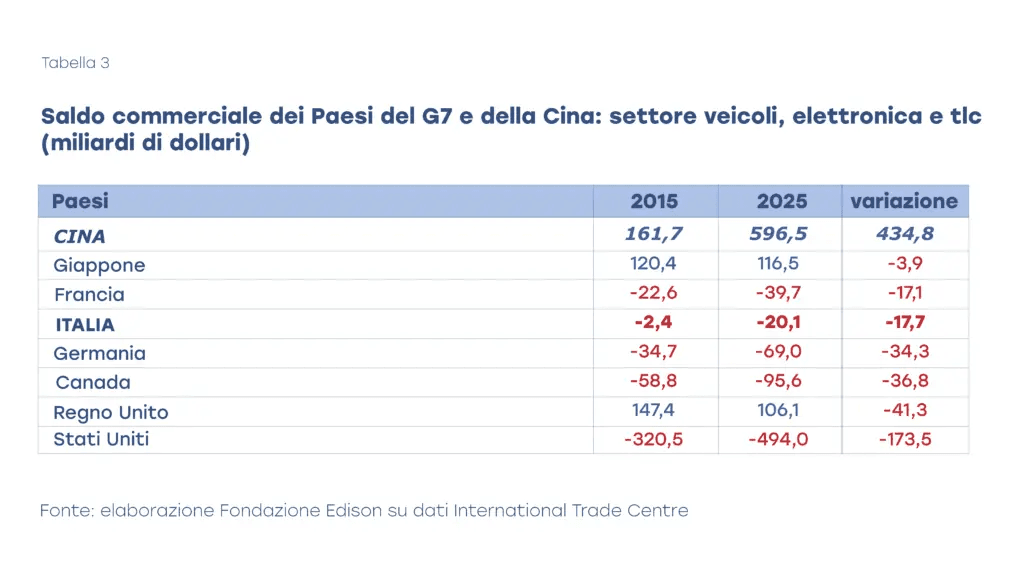

One can also observe the dynamics of the trade balances of the various countries in the automotive, electronics, and telecommunications sectors. China’s overall surplus in these sectors increased considerably from 2015 to 2025, by as much as 435 billion dollars. Japan’s surplus decreased slightly, while Germany’s, although still high, decreased over the decade by 41 billion. All other countries, particularly the United States, the United Kingdom, and Canada, saw their deficits worsen. Italy’s deficit grew by 17.7 billion.

Within this aggregate of sectors there is the item of vehicles and their parts. Chinese exports of vehicles and parts, excluding railway material, grew enormously from 2015 to 2025, rising from 63 billion dollars in 2015 to 248 billion in 2025. In this sector, China overtook Mexico in exports in 2021, Japan in 2022, and in 2025 came to less than 40 billion from Germany’s exports. The key to this planetary challenge is the growing leadership of the Asian giant in electric cars and related batteries. China’s foreign trade surplus in vehicles reached 207 billion dollars in 2025 and is now higher than both Germany’s, 130 billion, and Japan’s, 124 billion. It could soon exceed the sum of both.

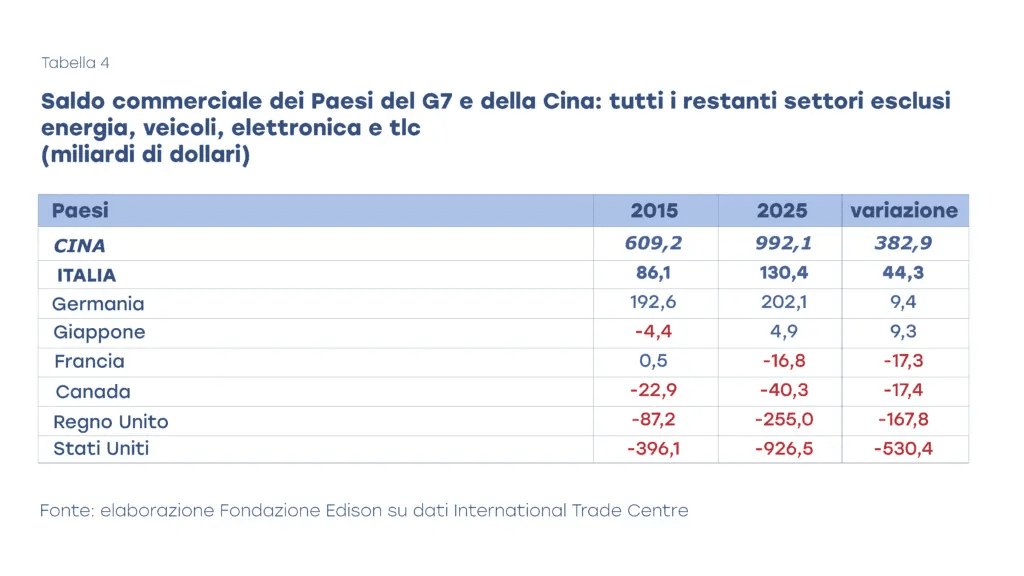

Finally, in the remaining sectors of world trade excluding energy, vehicles, and telecommunications, this imposing residual aggregate of products accounts for as much as 65% of total world exports and again sees China in the lead, with a surplus in 2025 of 992 billion dollars, up 383 billion compared with what Beijing had ten years earlier. The surprise here is Italy, which, thanks to the strength of its mechanical engineering, the resilience of its traditional fashion and furnishing sectors, the boom in pharmaceuticals, food and cosmetics, yachts and cruise ships, as well as aerospace, has become the world’s fourth-largest exporter in this residual category of goods, with a foreign surplus that increased by 44 billion in the last decade, reaching the extraordinary figure of 130 billion dollars.

How should we react to China’s growing overwhelming power? The European Union is caught between American tariffs, Chinese aggressiveness in the automotive sector, and the challenge of artificial intelligence, which both the United States and China are pushing toward boundaries beyond all imagination. China dominates the field of rare earths and batteries, and increasingly also that of raw materials for pharmaceuticals. The Old Continent appears stunned. Rapid decisions are urgently needed to contain the two superpowers, but Europe’s leading nation, Germany, appears uncertain about the strategy to pursue, as Tordoir and Setser underline in their report. France continues to hope that it can scrape by by selling Airbus planes and nuclear technologies to Beijing. The European Commission, partly for this reason, hesitates.

The Italian case is different. Can China really eat Made in Italy, as Corriere della Sera titled? We do not believe so. For now, Italy is defending its many specialization niches well, as shown by its growing trade surplus and by reaching, in less than ten years, the same export levels as a major country like Japan. Certainly, risks are not lacking. Apart from the incalculable damage to our companies from Chinese counterfeiting, which has continued uninterrupted since the beginning of the century, what is especially worrying is the blatant dumping that companies from the Asian giant are beginning to practice extensively, subsidized by their government, even on machinery and technologies in which Italy excels. In this case, the reality is not that our firms are no longer competitive, but that they are suffering clearly unfair competition. The response can only be one, as the footwear manufacturers did twenty years ago: to launch anti-dumping actions against China also in sectors such as mechanics, which Europe must absolutely support, without any reverential fear toward Beijing, also because by now Brussels has nothing left to lose.

We increase your company's long-term value

Discover our consulting services